Back to the Future II

The Scorecard, The War Nobody Priced, and Six Things You Can't Afford to Ignore

Life happens

Also

Better late than never

— a haiku from yours truly

Wishing everyone a very belated healthy and meaningful 2026!

Welcome back to the most irregularly published blog on the interwebs. Still no paid subscription. Still no passive income courses. Still no fin-fluencer status. My dreams of selling a masterclass on “How to Build Generational Wealth While Posting Market Commentary Once Every Year” remain firmly unrealised.

But here we are. And since I had the audacity to look back at my 2020 Supertanker Trends in last year’s Back to the Future post — and made some pretty clear calls about where each trend was heading — the only honest thing to do is score myself. Publicly.

Janus demands a mark to market.

“Prediction is very difficult, especially if it’s about the future.”

— Niels Bohr (a physicist, not a fund manager — but the point stands)

So let's do this. How did 2025 actually play out against the supertanker trends? And more importantly — as we sit here in the middle of 2026 with a Middle East war, oil still above $70, gold that briefly hit $5,600, Bitcoin in the $60s, and a Fed that's talking about hiking rates — where do we go from here?

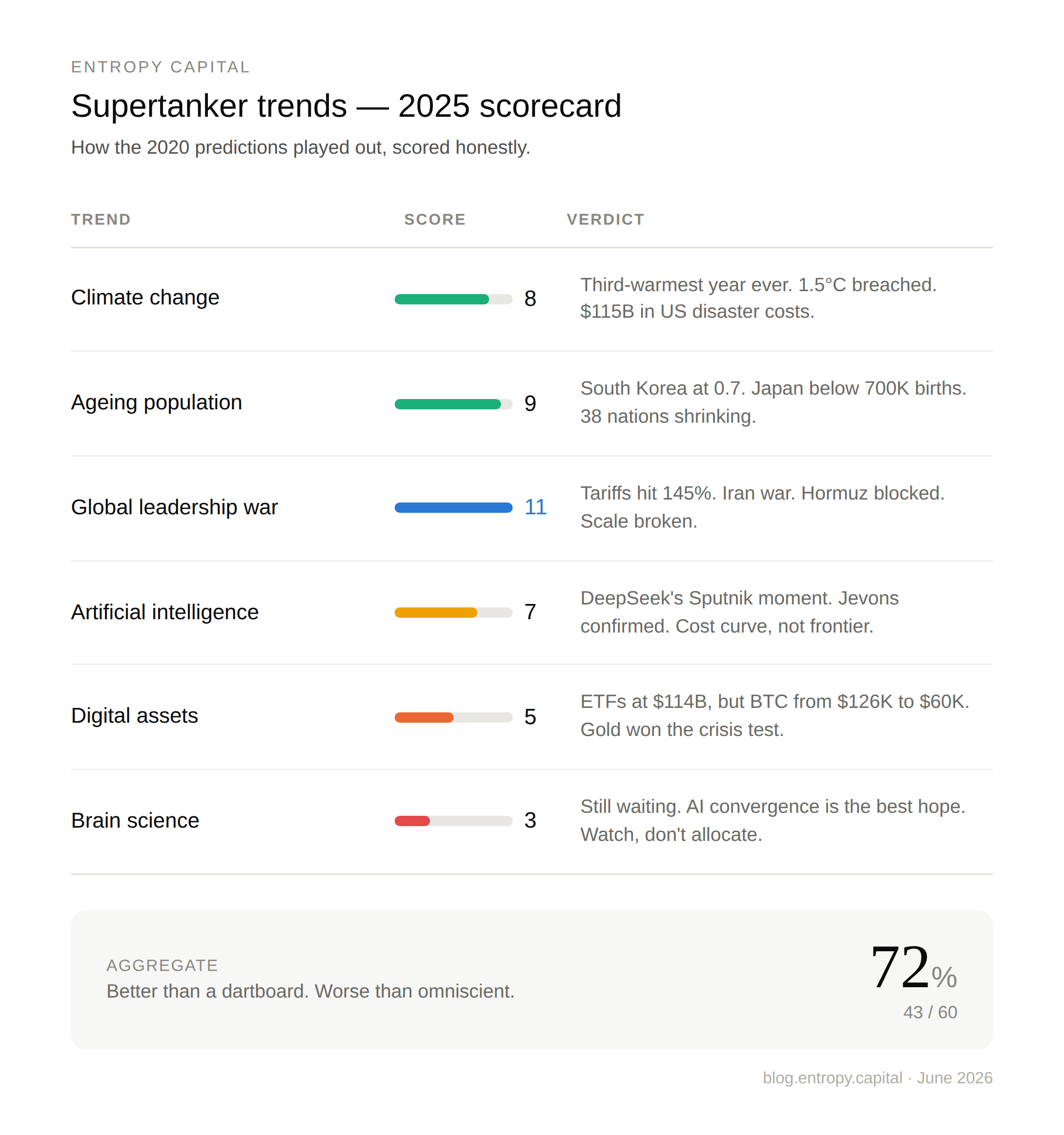

Trend #1 — Climate Change: Score 8/10

I said the trend would remain intact. I said greenwashing would continue at scale. I said regions would keep operating as factions, not as a species.

The data confirmed it — brutally. 2025 came in as the third-warmest year on record, with global surface temperatures 1.47°C above pre-industrial levels according to Copernicus. The last eleven years have now been the eleven warmest ever recorded. The three-year average from 2023-2025 has exceeded 1.5°C for the first time — the very threshold the Paris Agreement aimed to avoid.

Meanwhile, Antarctica recorded its warmest annual temperature ever. Arctic sea ice hit its lowest December extent in the satellite record. Europe logged its highest annual wildfire emissions on record. Weather-related disasters in the US alone caused $115 billion in damage across 23 events exceeding $1 billion each.

Although it is tempting to blame global warming for the latest massive heat wave in Europe this summer I still stand on the side of impartiality. It may be part of the global warming or it may be a statistical outlier. Or a new normal. Whatever it may be, it would extremely poor policy judgement to ignore this as part of a massive clear trend, man made or not.

The supertanker didn’t slow down. It accelerated. If anything, I underestimated how quickly the gap between rhetoric and reality would widen. The investment opportunities here — in adaptation infrastructure, catastrophe insurance, water technology, energy transition — are not hypothetical anymore.

Trend #2 — Ageing Population: Score 9/10

I flagged that the world might reach peak population earlier than expected. In 2025, the data became impossible to ignore.

South Korea’s fertility rate has collapsed to 0.7 births per woman — the lowest of any OECD nation and less than a third of the replacement level. China’s fertility sits at 1.0. Japan fell below 700,000 births for the first time in its history. Even the US slipped to 1.6. The global fertility rate now stands at approximately 2.1 — right at replacement level — with two-thirds of all countries already below that line.

The UN projects that 38 nations of more than one million people each will experience population decline over the next 25 years, up from 21 in the last 25 years. China alone is expected to lose 155 million people by 2050.

The longevity/fertility scissors are wide open and accelerating. This is not a trend you can reverse with a “baby bonus.” The implications for healthcare, robotics, pension systems, immigration policy, agriculture and consumer markets are massive. Every portfolio needs exposure to this theme — directly or indirectly. If you’re not thinking about this, you’re not thinking long term enough.

Trend #3 — Global Leadership War: Score 11/10

Yes, I’m breaking my own scale. Sue me.

If I had written a fictional screenplay of the 2025-2026 geopolitical landscape, my editor would have told me to tone it down for believability. And then the universe said, “Hold my beer.”

Act I: The Trade War. The US-China confrontation escalated to levels not seen in modern history. Tariffs on Chinese imports reached 145% at their peak before being walked back to around 30% after months of tit-for-tat escalation. China retaliated with its own tariffs, but more critically, deployed its rare earth mineral leverage — controlling roughly 60% of global production and 90% of rare earth magnet processing — forcing a genuine rethink of global supply chain vulnerability. The “Liberation Day” tariffs of April 2nd 2025 sent shockwaves through currency and equity markets. An eventual Trump-Xi meeting produced a short term truce. A pause, not a long term resolution.

Act II: The War. On February 28th 2026, the United States and Israel launched air strikes against Iran. Supreme Leader Khamenei was killed. Iran retaliated with hundreds of missiles and drones across the region — striking Israel, Gulf Arab states, and US military bases. Dubai International Airport was hit. And then came the card that risk models had always feared but never truly priced: Iran blocked the Strait of Hormuz.

Twenty percent of the world’s seaborne oil. Twenty-five percent of global LNG trade. Thirty percent of seaborne fertilizer trade. Gone overnight.

Brent crude spiked 64% in March alone — the largest monthly increase in oil prices ever recorded — peaking near $126 per barrel, with physical cargoes trading as high as $150. The IEA called it the largest supply disruption in the history of the world oil market. The 1970s energy crisis part II.

A ceasefire was signed on June 17th. As I write this, it remains fragile — Iran re-closed the strait days later citing Israeli violations in Lebanon, and over 500 vessels remain stranded in the Persian Gulf. The Strait is, as of this week, theoretically partially reopening via a US Navy-widened route near Oman. We shall see.

The market consequences have been profound. PCE inflation accelerated to 4.1% in May. The Fed is now talking about rate hikes. Gold hit an all-time high of $5,595 in January on pre-war tensions before correcting to around $4,040. Oil exporters outside the Gulf — particularly the US and Russia — have been the primary beneficiaries, while Persian Gulf producers that relied on Strait transit (Iraq, Kuwait, Qatar, UAE) saw revenues collapse.

Every investor now needs to price geopolitical risk as a first-order variable.

Trend #4 — Artificial Intelligence: Score 7/10

I said this was the trend that could impact all others. I said ignore it at your peril. Both statements proved prophetic. But I’ll be honest — even I didn’t see 2025 playing out quite like it did.

The DeepSeek Shock. On January 27th, a relatively obscure Chinese AI lab released a model that appeared to match Western frontier models at a fraction of the training cost. NVIDIA lost nearly $600 billion in market capitalisation in a single day — the largest one-day loss for any company in US stock market history. The Nasdaq plunged 3.1%. It was, in the words of many, “AI’s Sputnik moment.”

The core assumption — that US export controls on chips would maintain a durable American lead — was proven wrong. DeepSeek trained on weaker hardware and achieved comparable results. This didn't kill the AI bull case (NVIDIA ended 2025 up ~39% for the year, briefly touching a $5 trillion market cap in October, and hit a fresh all-time high of $236 in May 2026), but it fundamentally changed the narrative about AI moats, compute economics, and the geography of innovation.

Meanwhile, the Jevons Paradox played out beautifully. The cost to achieve a strong score on challenging AI benchmarks fell from $4,500 per task to $11.64 over the course of 2025. Did demand for compute decline? Absolutely not. More efficiency led to more usage, which led to more demand for infrastructure.

My score of 7/10 on myself is because while I correctly identified AI as the dominant meta-trend, I was too focused on the “will we reach AGI?” question and didn’t give enough weight to the democratization of AI capabilities and the geopolitical dimension of the race. The lesson: sometimes the most important developments happen not at the frontier but at the cost curve.

Trend #5 — Digital Assets: Score 5/10

Now this one humbles you. I was right on the structural thesis but the price action has been, to put it charitably, unkind.

The good news: institutional adoption surged. Spot Bitcoin ETFs ended 2025 with approximately $114 billion in total assets under management. BlackRock’s IBIT alone crossed $68 billion — holding over 800,000 BTC, more than MicroStrategy’s treasury. Over $34 billion flowed into crypto ETFs during 2025. A US Strategic Bitcoin Reserve was formally established. The SEC streamlined crypto ETF approvals from 270 days to 75 days.

The less good news: Bitcoin peaked near $126,000 in October 2025 and ended the year around $87,000. That’s pretty bad price action for a year that was supposed to be the blow-off top of the post-halving cycle. But 2026 has been worse. As I write this, Bitcoin is trading around $60,000 — down more than 50% from its highs. ETF outflows hit $2.7 billion in a single week in early June. Even MicroStrategy sold some BTC.

Meanwhile, in the category of “irony so thick you could trade it,” when the first real geopolitical crisis of this cycle arrived — a Middle East war, a blocked trade corridor, an oil shock, genuine fear — institutional and sovereign capital ran to the original safe haven, not the digital one. Gold hit $5,595. Bitcoin fell. The “digital gold” narrative met its stress test. It didn’t pass this time.

I give myself 5/10 because while my long-term thesis about blockchain, institutional adoption, and financial instruments becoming code is playing out exactly as described, the market doesn’t care about your thesis when there are missiles flying over the Strait of Hormuz. Bitcoin is increasingly correlated with risk assets and macro conditions. It’s growing up. Growing up means the easy money phase is over — and the “store of value in a crisis” badge still belongs to something that’s been doing the job for five thousand years.

Trend #6 — Brain Science: Score 3/10

I said in the original post that this trend hadn’t shown the breakthroughs I expected. A year and a half later? Still waiting. The link between consciousness and quantum mechanics that Sir Penrose discussed remains tantalizingly unresolved. There have been incremental advances in brain-computer interfaces and neurodegenerative disease research, but nothing transformational.

Interestingly, the convergence of AI and brain science may prove to be the key unlock — using AI to model neural patterns and accelerate our understanding of how the brain works, holistic human health and ultimately consciousness. But that’s still more potential than product for now.

Aggregate Scorecard: ~ 70%

Not bad for a second-tier blogger. But more importantly, the exercise of scoring yourself honestly is the whole point. Markets don’t care about your narrative. Neither should you once the outcomes have crystalized. It’s called reality check for a reason.

“When the facts change, I change my mind. What do you do, sir?”

— John Maynard Keynes

The Bold Calls: 2026 and Beyond

Alright, enough looking backwards. Janus has two faces for a reason. Here’s where I stick my neck out (again) for 2026 and beyond.

Prediction #1: The “AI Winter” Narrative Will Emerge — And Be Wrong

Expect to hear serious voices calling a plateau in AI. Rising debt levels at AI labs, questions about circular vendor financing (cloud companies buying AI, AI companies buying cloud), and the inevitable “where’s the ROI?” chorus from enterprise CFOs will fuel this narrative. Meanwhile NVIDIA, up only ~12% YTD while the broader semiconductor index is up 85%, will be cited as evidence that the trade is over.

It will feel compelling. It will be wrong. The Jevons Paradox isn’t done yet. AI inference costs will continue falling, unlocking use cases we haven’t imagined. The agentic AI wave — where AI systems don’t just answer questions but autonomously complete complex tasks — is just beginning. By 2027, AI agents will be managing significant portions of enterprise workflows, from code deployment to financial reconciliation. The compute buildout will surprise on the upside because of inference demand, not training demand.

Prediction #2: Geopolitics Will Keep Breaking Things in Financial Markets

When I first drafted this prediction earlier in 2026, I wrote: “I expect at least one major market dislocation in 2026 directly triggered by geopolitical events — likely involving supply chain disruption in semiconductors, energy, critical minerals or from private markets.”

A few weeks later, the United States went to war with Iran.

I was thinking semiconductors and rare earths. The universe delivered a blocked oil artery and a global energy shock instead. The lesson here is that geopolitical risk is no longer a tail risk. It’s the central scenario.

The Hormuz crisis has reshuffled the energy map. OPEC production has fallen 30%+. The UAE left OPEC and Iraq is thinking about leaving. Saudi Arabia and Oman are routing oil via pipelines and geography to bypass the Strait. The US and Russia — through sheer irony — are the biggest beneficiaries of the disruption. The post-war risk profile of Persian Gulf energy assets will be fundamentally different.

The US-China trade truce still expires. Europe faces an identity crisis between transatlantic alignment, strategic autonomy and self imposed regulatory purgatory. And now the Fed is contemplating rate hikes into a stagflationary oil shock. If you think the risk dislocations are over, you haven’t been paying attention.

Prediction #3: Bitcoin Will Print a New All-Time High — But Not How You Think

Let me be honest here. I predicted Bitcoin would reach new highs, driven by sovereign adoption. As of today, Bitcoin is at $60,000 and falling. The structural case remains — $114 billion in ETF assets, a US Strategic Reserve, growing institutional allocation — but the catalyst I expected hasn’t materialized the way I described.

What happened instead is instructive. When a real geopolitical crisis hit, capital didn’t flow to digital gold. It flowed to actual gold. Gold hit $5,595 in January 2026, a level that — for the first time — exceeded its 1980 inflation-adjusted high. That’s not just a safe haven bid. That’s genuine new price discovery for an asset with a five-thousand-year track record.

Bitcoin, meanwhile, is behaving like what it is (currently) : a high-beta risk asset that correlates with tech stocks during stress. That doesn’t make the long-term thesis wrong. The sovereign adoption angle is still nascent — China’s central bank bought gold at three times its prior rate in Q1 2026, and a record 45% of central banks plan to increase gold reserves this year. Bitcoin’s turn may come, but it comes after gold has re-established itself as the crisis asset of first resort.

I’m not abandoning this call. I’m adjusting the timeline. Expect the path to $150,000+ to take longer and go through deeper drawdowns than the crypto maximalists want to admit.

Prediction #4: The Demographic Cliff Will Become an Investment Theme

Demographics have been the most under-owned and under-discussed macro theme for years. That changes in 2026. As China’s population decline accelerates (155 million fewer people by 2050), Japan’s births crater, and even the US faces workforce contraction in key sectors, investors will scramble for exposure to automation, robotics, elder care technology, and longer term to immigration-friendly economies.

The countries and companies that solve the demographic equation — through AI-augmented productivity, immigration policy reform, or longevity technology — will be the compounders of the next decade. The ones that don’t will face fiscal crises that make current debt levels look quaint.

Prediction #5: Energy Is THE Bottleneck — And The War Proved It

I originally framed this as an AI-driven energy crunch. I wasn’t wrong about that — data-centre electricity demand is still growing exponentially — but the Iran war delivered the energy shock from a different direction entirely. And it’s worse than the AI scenario because it came with inflation attached.

Brent crude’s 64% spike in March was the largest monthly oil price increase in history. The Strait of Hormuz closure was the biggest disruption to world energy supply since the 1970s. Even with the ceasefire, the risk profile has permanently changed — Iran has demonstrated the will and capability to block the world’s most important energy chokepoint, and no amount of minesweeping restores the insurance market’s confidence overnight. Over 500 vessels remain stranded.

Nuclear energy’s renaissance is no longer theoretical. Small modular reactors, next-generation grid infrastructure, and energy storage are now critical national security investments, not just climate plays. The tension between AI’s insatiable energy appetite, climate commitments, and geopolitical reality will produce one of the great policy contradictions of our era.

Meanwhile, PCE inflation is running at 4.1% and the Fed is eyeing rate hikes. If you’ve been reading this blog, you know what that means: the stagflation scenario I’ve been discussing for years is no longer a scenario. It’s the base case. Positive equity-bond correlation. Duration compression. The 60/40 portfolio on life support. Pricing power as the primary equity screen. Real assets over financial assets.

Invest accordingly.

Prediction #6: The Great Rebalancing of Capital — Active Management Returns

A decade of passive dominance has created extraordinary concentration risk. The top 10 holdings in the S&P 500 represent a historically elevated share of the index. When geopolitics, AI disruption, demographic shifts, and a genuine energy crisis are simultaneously reshaping which companies and sectors win and lose, passive allocation becomes a bet on the status quo. The status quo is changing faster than at any point in modern market history.

The dispersion in 2026 is already extraordinary: oil producers vs oil consumers, defense vs travel, gold vs crypto, US energy exporters vs Gulf importers, companies with pricing power vs those without. The VanEck Semiconductor ETF is up 85% while NVIDIA is up 12%. Stock selection has never mattered more.

On a separate development linked to the AI thematic of Prediction #1: the latest models by OpenAI and Anthropic are doing a pretty decent job already as financial advisors (a topic to be explored in a future post). Passive management and basic active portfolio management is now almost fully commoditized and just survives by regulatory moats.

Active management — the disciplined, research-driven, risk-managed kind, not the “I have a hot tip” kind — will outperform in this environment. Stock-pickers, traders, contrarians, non-beta hedge funds, rejoice. Your decade is starting.

The Meta-Point

What connects all six of these predictions? Entropy. Not the nuisance kind that makes for good headlines and bad days. The structural kind that reshapes industries, creates and destroys fortunes, and rewards those who understood the supertanker trends before they became consensus.

The first half of 2026 has been a masterclass in what happens when multiple supertanker trends collide. Geopolitics met energy met inflation met AI met demographics — all at once, all in real time, all in your portfolio. The investors who had frameworks for this environment navigated it. The ones who were running 2019 playbooks in a 2026 world are nursing drawdowns and wondering what happened.

As I wrote back in 2020:

“Realization of the existence of a trend and acting upon it means exposure to assets and sectors that will be impacted long term by it. It also means actively managing liquid market risk, keeping your account healthy and yourself sane while still believing.”

That was true then. It’s even more true now. The trends haven’t changed direction. They’ve picked up speed. The question isn’t whether these trends matter — it’s whether you’re optimally positioned for what comes next.

“Follow the Trend Lines, Not the Headlines.”

— An important person that made a cameo in some recently released files

I occasionally share market commentary and random musings. None of this content should be taken as financial advice. Proceed at your own risk and DYOR.

Follow Entropy on WhatsApp and Telegram for occasional real time market snippets and on TradingView for infrequent charts like this.

Connect with me on LinkedIn.